RESTON, Va., May 6, 2024 /PRNewswire/ -- Broad Street Realty, Inc. (OTCQX: BRST)

To all our stakeholders.

At Broad Street, our vision has always been to strive "to empower people and places". What does this statement mean? It means that we have always emphasized a focus on the success of the businesses and entrepreneurs who occupy our essential grocery-anchored and mixed-use assets and the experience of their customers. Thankfully, this focus has rewarded us with the ability to weather both the Covid era and an incredibly difficult lending environment. Despite these stubborn headwinds, essential grocery-anchored shopping centers and student housing (our sole residential community) have performed remarkably well and have been viewed favorably by the lending and institutional investor community. This disciplined focus and our highly selective approach to essential shopping centers and mixed-use assets have given us financial advantages not available to other asset classes.

Last year, when I wrote this letter, I said "We have one major headwind in 2023: interest rates." Unfortunately, this was a very accurate statement and as of today, this condition has not changed. Credit is the lifeblood of a capital-intensive business such as that of commercial real estate ownership. It is no secret that the nation's lenders were challenged throughout 2023. We saw the closing of several major banks in the first half of last year. Large and middle market banks seemed to have slowly improved their balance sheets but still hesitate to lend, insurance companies have cherry picked the best assets at the lowest leverages, CMBS has been quiet, private equity is expensive. Our options have been limited.

Thanks to smaller banks and the insurers exhausting their cherry picking, the availability of debt capital has improved moderately as of the end of Q1 2024, but interest rates have not. In fact, they are approximately 95 basis points more expensive, as of the end of Q1 2024, than they were at this time in 2023. We have seen high volatility in interest rates -- improving and then widening again in very short time periods with dramatic swings. We had approximately $99.7 million of loans coming due last year. In order to address the expiring debt, we successfully refinanced the majority of it, extended one loan, and sold two shopping centers. The refinancing costs have not come cheaply.

As an example of our disciplined focus and selection process when we initially assembled our essential portfolio, I can point to the successful sale of two of our shopping centers last year. One was the Spotswood Valley Square Shopping Center in Harrisonburg, Virginia, and the other, Dekalb Plaza in suburban Philadelphia. Most of the proceeds were used to pay down a term loan and as reserves for capital needs at other assets.

It is true that both more expensive and limited availability of debt capital have a real impact on our cash flow and asset value. At the time we sold the two centers, interest rates were approximately 50 basis points better than in Q1 2024, and we achieved prices that were in line with our 2022 valuations. I am not sure we could duplicate that performance this year if we brought assets to market in this lending environment. Fortunately, we are not forced to sell anything at this time. Your guess is as good as mine as to when the Federal Reserve lowers rates, but it could not come soon enough so that we can take advantage of a lower cost of capital to improve our cash flow and our property valuations.

A quick summary of 2023 and more recent accomplishments:

- We resolved a majority of the $99.7 million of loans coming due by specifically having:

- Sold Spotswood Shopping Center, which retired $11.8 million in mortgage debt plus retiring a $2.3 million preferred interest.

- Sold Dekalb Plaza shopping center, retiring $17.4 million of mortgage debt.

- Refinanced four loans for a total of $45.3 million in proceeds, paying down $41.0 million of mortgage debt. These loans were secured by the Coral Hills, the Crestview Square, the Highlandtown Village, and the West Broad Commons shopping centers.

- In Q1 2024, we refinanced a loan of $11.3 million secured by the Vista Shops shopping center and in Q2 2024 a loan of $8.5 million secured by the Midtown Shopping Centers (identified in our public filings as Midtown Colonial and Midtown Lamonticello).

- We signed 74 leases for a total of 260,763 square feet of space, including 17 new leases for 41,360 square feet, 45 renewal leases for 197,144 square feet and 12 modifications for 22,259 square feet of our retail portfolio. Our total portfolio, including residential, was 90.1% leased at the end of 2023.

- Our leasing spread gains on both new and renewal leases demonstrate continued internal growth from our existing portfolio. In 2023, leasing spreads averaged 10.4%, including 35.9% for new leases and 7.7% on renewals.

- Midtown Row Residential was 100% leased for the 2023-2024 academic school year. The annualized base rental revenue per square foot in 2023 was 1.7% higher than 2022. As of April 30, 2024, Midtown Row Residential is 100% pre-leased for the 2024-2025 academic year with healthy ABR (Annualized Base Rent) growth.

- Reported net loss of $7.0 million, funds from operations ("FFO") attributable to common stockholders and OP unit holders of $2.4 million and adjusted FFO ("AFFO") attributable to common stockholders and OP unit holders of $3.0 million. See "Non-GAAP Performance Measures" at the end of this press release.

- Reported net operating income ("NOI") of $24.9 million and same-center NOI of $15.9 million — an increase of 5.6% over the prior year. See "Non-GAAP Performance Measures" at the end of this press release.

- Revenues for the year ended December 31, 2023, increased approximately $9.2 million, or 28%, from the prior year because of an approximately $9.1 million and $0.4 million increase in rental income and commissions, respectively, partially offset by an approximately $0.3 million decrease in management and other income.

- Increase in rental income is attributable to the acquisition of two properties in the fourth quarter of 2022, partially offset by the disposition of two properties during 2023.

- The increase in commissions is attributable to higher transaction volume in leasing. The decrease in management and other income is mainly attributable to fees recognized in 2022 related to properties that were acquired in 2022.

Most of our portfolio is concentrated towards grocery, essential retail, daily needs, and value-oriented tenants that require customers to physically visit the location to receive goods and services. The benefit of this tenant mix is borne out in our revenue, leasing momentum, improving leasing spreads and WALT ("weighted average lease term").

A few further highlights from the portfolio speak to the quality and performance of our tenants as well as the efforts of our leasing and asset management staff:

- We proactively renewed multiple key anchors throughout the portfolio including improving our WALT and our ABR.

- Casa Bonita re-opened at Lamar Station in Lakewood Colorado to a long waiting list, in addition to Arc Thrift.

- An AutoZone mega hub opened at Cromwell Shopping Center in Glen Burnie Maryland.

- At Midtown Row, we held numerous well-attended events at our Village Green that were widely supported by our tenants and helped leasing efforts. Grit Coffee, Riverside Healthcare, and Cook's Burger Bar opened to much fanfare.

- Although we cannot report the figures, many of our essential anchors report sales to us, and most showed continued improvement in 2023.

Our fine Broad Street real estate services team offers primarily tenant representation services to both office and retail tenants throughout the Washington, D.C. metro area and the Denver, Colorado markets. In 2023, they successfully represented emerging office and retail tenants such as Vint Hill Solutions, Laconiko, Greater Washington Board of Trade, RLJ Equity Partners, Target, Boston University, Tennessee Valley Authority, Dutch Brothers, NMA, United States Navy Memorial Foundation. They have also had some great recent customer wins that I look forward to sharing later in 2024.

We have an incredibly focused staff and company culture. Our core "TRIBAL" values (Teamwork, Respect, Integrity, Balance, Accountability and Leadership) are reinforced with 30 key behavioral fundamentals that we teach, reward, and reinforce each week at Broad Street. This focus on a conscious culture helps our staff work together, solve problems, achieve, and drive company performance. I am very proud of my colleagues' efforts.

As you can tell, we had a busy 2023 and start to 2024. Thanks to our incredibly dedicated staff, we conquered our most significant challenge, which was the refinancing and paydown of $99.7 million of expiring debt. By almost every data measure, we improved the portfolio performance and improved our balance sheet. We are pursuing, with vigor, several strategic pathways forward. Hope is not a strategy. So we cannot hope for better capital markets moving forward. We believe in our great essential grocery-anchored and mixed-use asset portfolio and focus on essential businesses and services provide us a significant strategic advantage and opportunity. Our success in our pursuits will be driven not by hope but by focus, discipline, and a conscious choice to succeed.

About Broad Street Realty, Inc.

Broad Street Realty, Inc. is a fully integrated and self-managed real estate company that owns, operates, develops, and redevelops primarily essential grocery-anchored shopping centers and mixed-use properties located in densely populated technology employment hubs and higher education centers within the Mid-Atlantic, Southeast and Colorado markets. Broad Street is also a market-leading commercial real estate services firm that delivers cost-effective solutions for office, industrial and retail clients.

Forward-Looking Statements

This press release contains forward-looking statements within the meaning of the U.S. federal securities laws. These forward-looking statements include, without limitation, statements about our estimates, expectations, predictions and forecasts of our future business plans and financial and operating performance and/or results, as well as statements of management's goals and objectives, future acquisitions and other similar expressions concerning matters that are not historical facts. When we use the words "may," "should," "could," "would," "predicts," "potential," "continue," "expects," "anticipates," "future," "intends," "plans," "believes," "estimates" or similar expressions or their negatives, as well as statements in future tense, we intend to identify forward-looking statements. Although we believe that the expectations reflected in such forward-looking statements are based upon reasonable assumptions, beliefs and expectations, such information is necessarily subject to uncertainties and may involve certain risks, many of which are difficult to predict and are beyond the control of the Company's management. These risks include, but are not limited to: the Company's limited access to capital and its ability to repay, refinance, restructure and/or extend its indebtedness as it becomes due; the Company's success in implementing its business strategy and its ability to identify, underwrite, finance, consummate and integrate acquisitions or investments; adverse economic or real estate developments, either nationally or in the markets in which the Company's properties are located; changes in financial markets and interest rates, or to the Company's business or financial condition; the nature and extent of competition; other factors affecting the retail industry or the real estate industry generally; the performance of the Company's portfolio; the impact of any financial, accounting, legal or regulatory issues or litigation; and other risks that are set forth under "Risk Factors" in the Company's Annual Report on Form 10-K for the year ended December 31, 2023, and other documents filed by the Company with the Securities and Exchange Commission from time to time. All forward-looking statements speak only as of the date of this press release. All subsequent written and oral forward-looking statements attributable to us or any person acting on our behalf are qualified by the cautionary statements in this section. Except as otherwise may be required by law, the Company undertakes no obligation to update or publicly release any revisions to forward-looking statements to reflect events, circumstances, or changes in expectations after the date of this press release.

Non-GAAP Performance Measures

We present the non-GAAP performance measures set forth below. These measures should not be considered as an alternative to, or more meaningful than, net income (calculated in accordance with GAAP) or other GAAP financial measures, as an indicator of financial performance and are not alternatives to, or more meaningful than, cash flow from operating activities (calculated in accordance with GAAP) as a measure of liquidity. Non-GAAP performance measures have limitations as they do not include all items of income and expense that affect operations, and accordingly, should always be considered as supplemental financial results to those calculated in accordance with GAAP. Our computation of these non-GAAP performance measures may differ in certain respects from the methodology utilized by other real estate companies and, therefore, may not be comparable to similarly titled measures presented by other real estate companies. Investors are cautioned that items excluded from these non-GAAP performance measures are relevant to understanding and addressing financial performance.

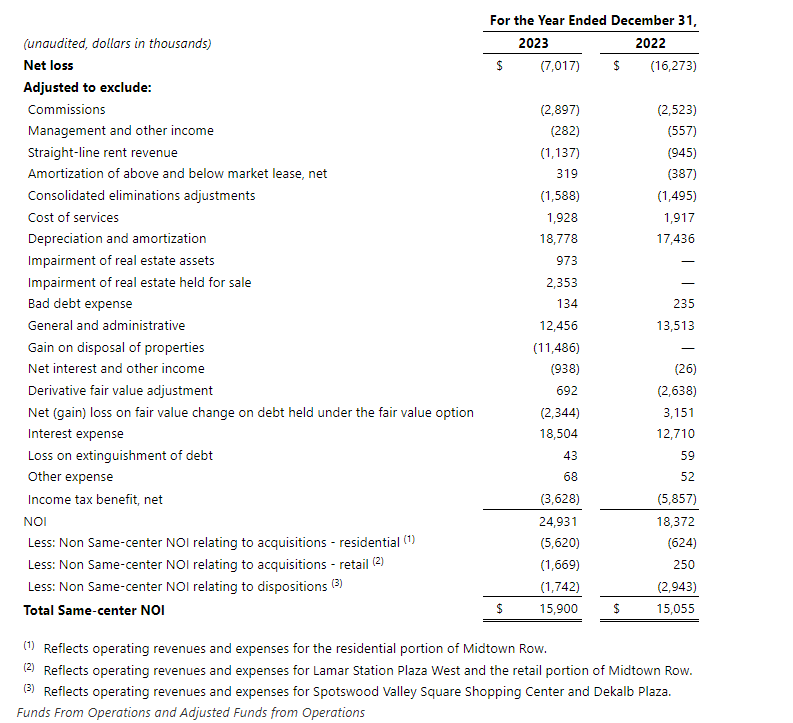

Net Operating Income and Same-center Net Operating Income

NOI is a supplemental non-GAAP measure of the operating performance of our properties. We define NOI as rental income less property operating expenses, including real estate taxes. We also exclude the impact of straight‑line rent revenue, net amortization of above and below market leases, depreciation and amortization, interest, impairments and gains or losses of real estate assets and other significant infrequent items that create volatility in our earnings and make it difficult to determine the earnings generated by our core ongoing business. Same-center NOI should not be viewed as an alternative measure to net income or loss calculated in accordance with GAAP as a measurement of our financial performance. We believe that NOI is a helpful measure because it provides additional information to allow management, investors and our current and potential creditors to evaluate and compare our core operating results.

Same-center NOI is a supplemental non-GAAP financial measure which we use to assess our operating results. For the years ended December 31, 2023 and 2022, Same-center NOI represents the NOI for thirteen properties that were wholly owned and operational for the entire portion of each reporting period. Same-center NOI should not be viewed as an alternative measure to net income or loss calculated in accordance with GAAP as a measurement of our financial performance, as it does not reflect the operations of our entire portfolio. We believe that Same-center NOI is a helpful measure because it provides additional information to allow management, investors and our current and potential creditors to enhance the comparability of our operating performance between periods.

The table below compares Same-center NOI for the years ended December 31, 2023 and 2022:

Our reconciliation of Same-center NOI for the years ended December 31, 2023, and 2022 is as follows:

Funds from operations ("FFO") is a supplemental non-GAAP financial measure of real estate companies' operating performance. The National Association of Real Estate Investment Trusts ("Nareit") defines FFO as follows: net income (loss), computed in accordance with GAAP, excluding (i) depreciation and amortization related to real estate, (ii) gains and losses from the sale of certain real estate assets, (iii) gains and losses from change in control, (iv) impairment write-downs of certain real estate assets and investments in entities when the impairment is directly attributable to decreases in the value of depreciable real estate held by the entity and (v) after adjustments for unconsolidated partnerships and joint ventures calculated to reflect FFO on the same basis.

Historical cost accounting for real estate assets in accordance with GAAP implicitly assumes that the value of real estate assets diminishes predictably over time. Since real estate values instead have historically risen or fallen with market conditions, many industry investors and analysts have considered the presentation of operating results for real estate companies that use historical cost accounting to be insufficient by themselves. Considering the nature of our business as a real estate owner and operator, we believe that FFO is useful to investors in measuring our operating and financial performance because the definition excludes items included in net income that do not relate to or are not indicative of our operating and financial performance, such as depreciation and amortization related to real estate, and items which can make periodic and peer analysis of operating and financial performance more difficult, such as gains and losses from the sale of certain real estate assets and impairment write-downs of certain real estate assets. Specifically, in excluding real estate related depreciation and amortization and gains and losses from sales of depreciable operating properties, which do not relate to or are not indicative of operating performance, FFO provides a performance measure that, when compared year over year, captures trends in occupancy rates, rental rates and operating costs.

However, because FFO excludes depreciation and amortization and captures neither the changes in the value of our properties that result from use or market conditions nor the level of capital expenditures and leasing commissions necessary to maintain the operating performance of our properties, all of which have real economic effects and could materially impact our results from operations, the utility of FFO as a measure of our performance is limited. Accordingly, FFO should be considered only as a supplement to net income as a measure of our performance. FFO should not be used as a measure of our liquidity, nor is it indicative of funds available to fund our cash needs, including our ability to pay dividends or service indebtedness. Also, FFO should not be used as a supplement to or substitute for cash flow from operating activities computed in accordance with GAAP.

Adjusted FFO ("AFFO") is calculated by excluding the effect of certain items that do not reflect ongoing property operations, including stock-based compensation expense, deferred financing and debt issuance cost amortization, non-real estate depreciation and amortization, straight-line rent, non-cash interest expense and other non-comparable or non-operating items. Management considers AFFO a useful supplemental performance metric for investors as it is more indicative of the Company's operational performance than FFO.

AFFO is not intended to represent cash flow or liquidity for the period and is only intended to provide an additional measure of our operating performance. We believe that Net income/(loss) is the most directly comparable GAAP financial measure to AFFO. Management believes that AFFO is a widely recognized measure of the operations of real estate companies, and presenting AFFO enables investors to assess our performance in comparison to other real estate companies. AFFO should not be considered as an alternative to net income/(loss) (determined in accordance with GAAP) as an indication of financial performance, or as an alternative to cash flow from operating activities (determined in accordance with GAAP) as a measure of our liquidity, nor is it indicative of funds available to fund our cash needs, including our ability to make distributions.

Our reconciliation of net income (loss) to FFO and AFFO for the years ended December 31, 2023, and 2022 is as follows:

| For the Year Ended December 31, | ||||||||

| (dollars in thousands) | 2023 | 2022 | ||||||

| Net loss | $ | (7,017) | $ | (16,273) | ||||

| Gain on disposal of properties | (11,486) | — | ||||||

| Impairment of real estate assets held for sale | 2,353 | — | ||||||

| Real estate depreciation and amortization | 18,425 | 17,259 | ||||||

| Amortization of direct leasing costs | 109 | 44 | ||||||

| FFO attributable to common shares and OP units | 2,384 | 1,030 | ||||||

| Stock-based compensation expense | 1,477 | 1,937 | ||||||

| Deferred financing and debt issuance cost amortization | 834 | 1,512 | ||||||

| Impairment of real estate assets | 973 | — | ||||||

| Intangibles amortization | 319 | (387) | ||||||

| Non-real estate depreciation and amortization | 244 | 131 | ||||||

| Non-cash interest expense | 1,253 | 253 | ||||||

| Recurring capital expenditures | (1,347) | (981) | ||||||

| Straight-line rent revenue | (1,137) | (945) | ||||||

| Minimum return on preferred interests | (331) | (1,112) | ||||||

| Non-cash fair value adjustment | (1,652) | 513 | ||||||

| AFFO attributable to common shares and OP units | $ | 3,017 | $ | 1,951 | ||||

| Weighted average shares outstanding to common shares | ||||||||

| Diluted | 35,608,163 | 32,378,526 | ||||||

| Earnings per share of common stock | ||||||||

| Net loss per share attributable to stockholders - diluted (1) | $ | (0.60) | $ | (0.47) | ||||

| Weighted average shares outstanding to common shares and OP units | ||||||||

| Diluted | 41,168,459 | 35,412,984 | ||||||

| FFO per common share and OP unit | ||||||||

| Diluted (2) | $ | 0.06 | $ | 0.03 | ||||

| (1) | The weighted average common shares outstanding used to compute net loss per diluted common share only includes the common shares. We have excluded the OP units since the conversion of OP units is anti-dilutive in the computation of diluted EPS for the periods presented. |

| (2) | The weighted average common shares outstanding used to compute FFO per diluted common share includes OP units that were excluded from the computation of diluted EPS. Conversion of these OP units is dilutive in the computation of FFO per diluted common share but is anti-dilutive for the computation of diluted EPS for the periods presented. |

SOURCE Broad Street Realty, Inc.

For further information: Mylisha Palmer, mpalmer@broadstreetrealty.com

Leave a Reply